Covid-19. Legal and Financial Tools at the disposal of enterprises, how to deal with an emergency.

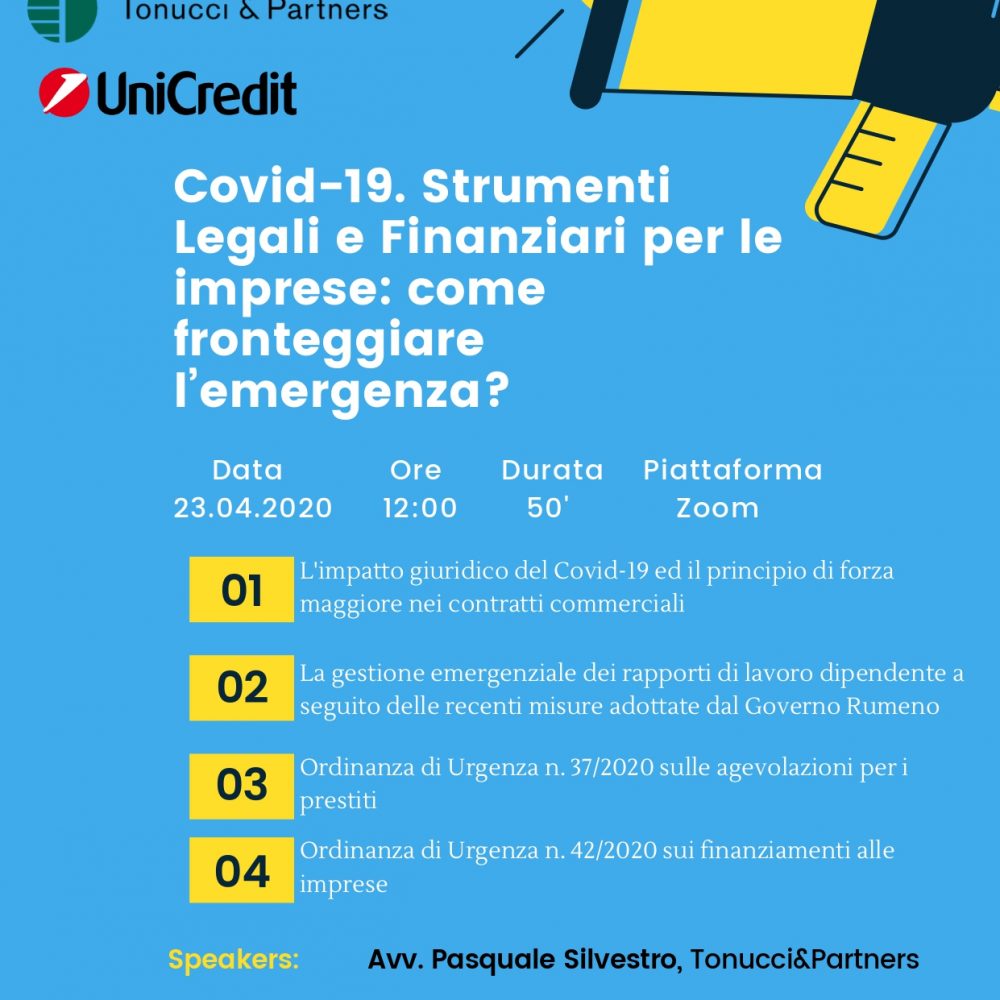

Tonucci & Partners, with Pasquale Silvestro and in collaboration with the Italian Chamber of Commerce for Romania and

Tonucci & Partners, with Pasquale Silvestro and in collaboration with the Italian Chamber of Commerce for Romania and

Contribution by Alessandro Vasta of Tonucci & Partners on societàerischio.it with the article “Do Covid 19 App actually

Contribution by Paola Salvi of Tonucci & Partners, expert in Family Law, on Io Donna – RCS Media

Contribution of Alessandro del Ninno regarding a primary analysis – based on the available information – related to

The Supreme Court of Cassation, by decision n. 11626 of 07.04.2020, ruled on a highly debated issue since the entry into force of the Legislative Decree no. 231/2001 stating that foreign legal entities, without offices in Italy, may be held liable for criminal offences committed in the Italian territory.

Contribution of Alessandro Del Ninno regarding a primary analysis – based on the available information – related to

The Supreme Court has recently stated, although in obiter dictum, that it is possible for the purchaser of shares to resolve the termination of the contract of the sale because of the different economic consistency of the company whose shares have been sold compared to that which was declared by the seller.

Tonucci & Partners, with Pasquale Silvestro and in collaboration with the Italian Chamber of Commerce for Romania and

L’Avv. Alessandro del Ninno di Tonucci & Partners ha pubblicato su Diritto & Giustizia di Giuffrè Lefebvre Editore

In this interview released to the daily magazine online Key4biz, Alessandro del Ninno of Tonucci & Partners points

Tonucci & Partners has prepared a brief Memo on social safety nets during Covid-19 emergency. The Memo draws

During the last plenary session held on April 7, 2020, the European Data Protection Board (EDPB) entrusted its expert committees with the task of identifying and developing the relevant principles regarding the processing of personal data in the context of the containment of the COVID-19 virus through the approval of two specific mandates, concerning respectively the tracking and geolocation tools and the processing of health data for research purposes.